Brazil is one of the largest economies in Latin America and a compelling destination for international investors. With a consumer market of over 215 million people, diversified industries, and GDP growth of approximately 2.5% in 2025 (IBGE data), the country offers significant opportunities across sectors ranging from technology and agribusiness to financial services and manufacturing.

One of the most common questions among foreign investors is whether it is possible to open or participate in a company in Brazil, and what legal requirements must be met.

This guide answers those questions and more to help you navigate the path from planning to operation.

Yes. Brazilian law allows companies incorporated in the country to be entirely owned by foreign individuals or foreign legal entities. Unlike some jurisdictions, Brazilian corporate law generally does not require the participation of Brazilian partners in the ownership structure.

This means foreign investors can establish and fully control a Brazilian company, provided that applicable legal and regulatory requirements are fulfilled including tax identification, legal representation in Brazil, document legalization, and registration of foreign investment with the Central Bank of Brazil.

The LTDA is the most widely used corporate structure in Brazil. It offers contractual flexibility, relatively simple administration, and limited liability for partners; meaning their liability is restricted to the value of their capital contributions. This structure is ideal for small to mid-sized foreign-owned operations.

The S.A. structure is typically used for larger operations or projects that require a more sophisticated corporate governance framework, as well as the potential to raise capital through investors or capital markets. It carries slightly higher setup and compliance costs but offers greater scalability.

In Brazil, both individuals and companies must obtain tax identification numbers in order to conduct business activities and interact with government authorities.

The CPF is the tax identification number assigned to individuals by the Brazilian Federal Revenue Service (Receita Federal do Brasil). Foreign investors who wish to become partners or shareholders in Brazilian companies must obtain a valid CPF.

Importantly, foreigners do not need to reside in Brazil in order to obtain a CPF. This registration is required for:

• Participating as a shareholder or partner in a Brazilian company

• Signing corporate documents

• Performing acts before Brazilian administrative and tax authorities

Processing Time: A CPF can typically be obtained within 1–2 weeks via online application through the Receita Federal portal. Foreigners can also apply at Brazilian consulates abroad.

The CNPJ is the tax identification number assigned to companies incorporated in Brazil. Once the company is formally incorporated and its corporate documents are registered with the competent Commercial Registry (Junta Comercial), the Brazilian Federal Revenue Service issues the company's CNPJ number.

With the CNPJ, the company can:

• Issue invoices (Notas Fiscais)

• Open corporate bank accounts

• Hire employees and register with labour authorities

• Comply with federal, state, and municipal tax obligations

Yes. Brazilian legislation requires foreign investors participating in Brazilian companies to appoint a legal representative who resides in Brazil. This representative acts as the official point of contact between the foreign investor and Brazilian authorities.

Their responsibilities include:

• Receiving administrative or judicial notifications on behalf of the investor

• Representing the investor before public authorities when necessary

• Signing certain corporate and regulatory documents

The appointment is made through a Power of Attorney, granting specific powers to the representative. This document must be signed abroad, apostilled in accordance with the Hague Apostille Convention, and translated into Portuguese by a sworn translator in Brazil.

Additionally, Brazilian corporate law requires that the company itself appoint at least one administrator who resides in Brazil.

Here is a practical overview of the typical incorporation process for a foreign-owned LTDA in Brazil:

Conduct market analysis, identify applicable sector regulations (some industries have specific foreign ownership restrictions), and define the company's corporate purpose (objeto social).

All foreign shareholders must obtain a CPF before the company can be incorporated. This can be done through Brazilian consulates abroad or online via the Receita Federal portal.

Draft the Articles of Association (Contrato Social for LTDA), appoint a resident administrator, and prepare the Power of Attorney for the foreign investor's Brazilian legal representative. All foreign documents must be apostilled and translated by a sworn translator.

Submit the articles of incorporation and supporting documents. Pay the applicable registration fees (approximately R$200–R$500 depending on the state). Processing typically takes 5–10 business days.

After Junta Comercial approval, register the company with the Federal Revenue Service to obtain the CNPJ. This is done via the REDESIM portal and is often processed simultaneously with commercial registration in many states.

Obtain municipal business licenses (Alvará de Funcionamento), register with state tax authorities for ICMS if applicable, open a corporate bank account, and register the foreign investment with the Central Bank of Brazil (BACEN) via the RDE-IED module.

Estimated Timeline: 1–3 months for a standard LTDA incorporation. Engaging experienced local counsel can significantly reduce this timeframe.

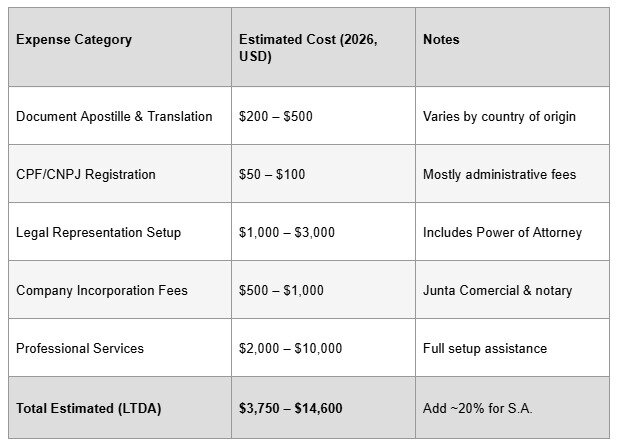

The table below provides estimated costs for a basic LTDA incorporation in Brazil as of 2026. Costs can vary depending on the state of incorporation, the complexity of the corporate structure, and the professional services engaged.

Foreign investors are not required to reside in Brazil to own or manage a Brazilian company. However, obtaining a visa or residency can facilitate day-to-day management and simplify interactions with local authorities. The main options include:

• Investor Visa: For investments of at least R$500,000 in a Brazilian company. Grants a temporary residence permit, renewable upon proof of ongoing investment.

• Tech Visa: Designed for professionals in technology and innovation. Useful for founders of tech startups.

• Permanent Residency: Available after a period of temporary residency or through qualifying investments.

• Digital Nomad Visa: Available since 2022 for remote workers with no minimum investment requirement — popular among founders in the early stages of a Brazilian venture.

• VITEM V (Temporary Work Visa): Available to directors and administrators of Brazilian companies who require active involvement in day-to-day operations.

Brazil's corporate tax system can be complex, with overlapping federal, state, and municipal taxes. The main taxes applicable to companies include:

• IRPJ (Corporate Income Tax): 15% on taxable income, plus a 10% surtax on annual profits exceeding R$240,000 — resulting in an effective rate of approximately 25%.

• CSLL (Social Contribution on Net Income): 9% for most companies, bringing the total federal income tax burden to approximately 34%.

• PIS/COFINS (Social Contributions on Revenue): Rates vary between the cumulative and non-cumulative regimes (0.65%/3% or 1.65%/7.6% respectively).

• ICMS (State VAT): Rates vary by state and product/service category, ranging from 7% to 18%.

• ISS (Municipal Service Tax): 2% to 5% on services provided.

Brazilian companies can choose from three main tax regimes:

• Simples Nacional: Simplified regime for small businesses with annual revenue up to R$4.8 million. A single monthly payment covers most federal, state, and municipal taxes.

• Lucro Presumido: Presumed profit regime for companies with annual revenue up to R$78 million. Tax is calculated on a fixed percentage of gross revenue.

• Lucro Real: Actual profit regime, mandatory for larger companies or financial institutions. Tax is calculated on actual net profits after deductions.

• Regional Incentives: Companies operating in the Amazon region (SUFRAMA) or the Northeast (SUDENE/ADENE) may qualify for income tax reductions of up to 75%.

• R&D Credits: The Brazilian Innovation Law (Lei do Bem) provides tax deductions of 60–80% on qualifying R&D expenditures for companies in the Lucro Real regime.

• PROEX Program: Supports Brazilian exporters with up to 100% financing for eligible businesses.

• Double Taxation Treaties: Brazil has tax treaties with over 30 countries. Investors should verify whether their home country has a treaty with Brazil to avoid double taxation.

Brazil is a rewarding market, but it comes with its own set of business complexities. Being aware of these challenges in advance allows for better planning:

• Bureaucracy: Brazil's regulatory environment involves multiple layers of federal, state, and municipal requirements. Solution: Engage experienced local legal and accounting professionals from the outset.

• Currency Fluctuations: The Brazilian Real (BRL) can be volatile. Solution: Use currency hedging tools and monitor exchange rates carefully when planning capital injections.

• Tax Complexity: Brazil's tax system is among the most complex in the world. Solution: Work with a local tax advisor to select the optimal tax regime and ensure ongoing compliance.

• Cultural and Language Differences: Business culture in Brazil places high value on personal relationships and trust. Solution: Partner with bilingual advisors who understand both local and international business practices.

• Banking Access: Opening a corporate bank account can be lengthy for foreign-owned companies. Solution: Prepare all documentation in advance and work with a service provider experienced in this process.

Typically 1–2 weeks via online application through the Receita Federal portal. Applications can also be made at Brazilian consulates abroad.

Yes. Certain sectors have specific restrictions or require prior authorisation, including nuclear energy, rural land ownership, certain media activities, and health-related businesses regulated by ANVISA. It is important to verify sector-specific regulations before structuring your investment.

Yes. Foreign direct investment must be registered with the Central Bank of Brazil (BACEN) via the RDE-IED module of the SISBACEN system. This registration is important for the future repatriation of profits and capital.

Yes. From 2021, the LTDA can be constituted by a single partner (Sociedade Limitada Unipessoal — SLU), allowing a sole foreign individual to own and operate a Brazilian company without needing a second partner.

Yes, provided that the company has at least one administrator residing in Brazil, and that the foreign investor has appointed a Brazilian legal representative via a duly apostilled Power of Attorney.

While Brazil offers significant opportunities for international investors, establishing a company in the country requires careful planning and compliance with local legal and regulatory requirements. Proper structuring from the beginning ensures legal certainty, tax efficiency, and smoother operations.

JJ Associates assists international clients throughout the entire process of establishing and structuring companies in Brazil, including:

• Company incorporation (LTDA, S.A., and SLU)

• CPF registration for foreign partners

• Tax registration and regulatory compliance

• Legal representation for foreign investors

• Power of Attorney drafting and apostille coordination

• Corporate governance and legal advisory

• Assistance with banking and operational setup

• Registration of foreign investment with BACEN

If you are considering expanding your business to Brazil, our team will be pleased to guide you through each step of the process. Contact JJ Associates for a personalised consultation.

Have a question?

Company address:

Tower Financial Center, 28th Floor, Office F, Calle 50, Ciudad de Panama, Panama.Follow us